“Each mRNA pioneer should evaluate their substantial patent portfolios to determine which existing patents are enforceable against other market players . . . [and] analyze their existing patent applications to determine whether broad claims can be written to cover current or anticipated competitor activity.”

In Part I of this series providing a summary of the mRNA IP and competitive landscape through one year of the COVID-19 pandemic, we focused on market players BioNTech, Moderna and CureVac; in Part II, we discussed Translate BIO, Arcturus, and eTheRNA (and other startups) and provided background on activity relating to certain Arbutus lipid nanoparticle (LNP) delivery technology.

Here, in our final post, we provide an analysis of the current landscape and offer conclusions.

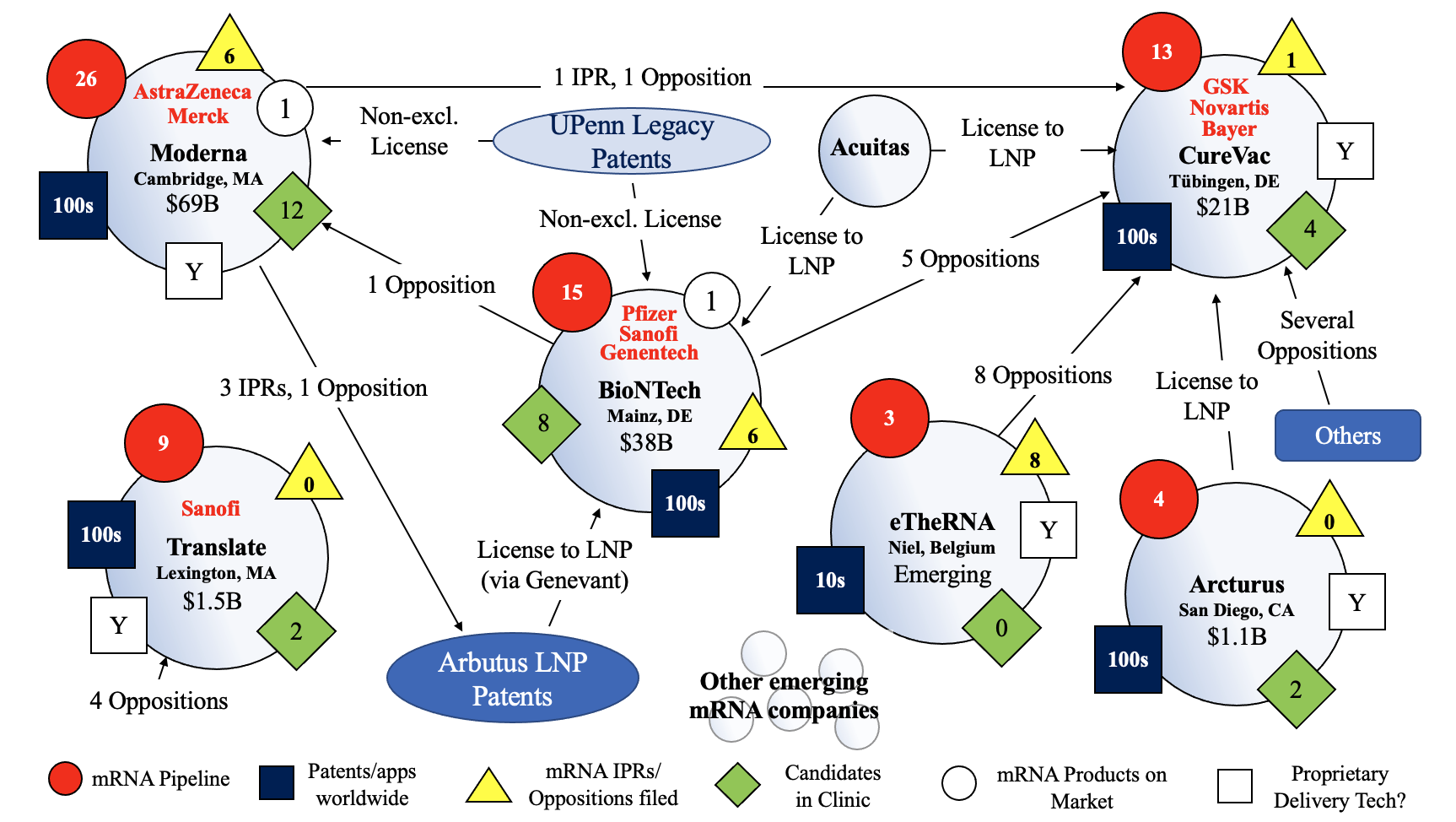

Moderna, BioNTech and CureVac –Leading Pioneers

The three largest and best-positioned players in the mRNA space are currently Moderna, BioNTech and CureVac, each having very large patent estates, 11-figure market caps, double-digit candidates in their pipelines, years of development work and accumulated know-how under their belts, and key licenses and other strategic alliances in place for the manufacture, development, and commercialization of mRNA-based products. Moderna and BioNTech (with Pfizer) have each broken through certain regulatory barriers for mRNA with the approvals to commercialize their respective COVID-19 vaccine products, and CureVac is apparently not far behind with a COVID-19 vaccine of its own in Phase 3 clinical trials.

Moderna and BioNTech each appear to benefit from non-exclusive sublicenses to UPenn’s legacy mRNA technology, but the core terms of those agreements are not publicly known. While at least one of the UPenn patents appears to have broad claims, it is not clear how strong those claims are or whether others in the mRNA space need UPenn’s patents to operate. For example, it is not clear whether CureVac in-licenses UPenn’s legacy mRNA technology, or needs to. CureVac has already had one UPenn patent revoked in Europe, but there is no record of CureVac or any other party filing an inter partes review (IPR) with respect to UPenn’s ‘036 patent.

BioNTech and Moderna have each been somewhat active in seeking to invalidate competitor patents, with BioNTech filing oppositions against one Moderna patent and five CureVac patents, and Moderna filing three IPRs and one opposition against four Arbutus patents and one opposition against a CureVac patent. CureVac, on the other hand, appears not to have directly attacked its competitors’ patents to date, at least in a manner that is publicly known. Expect to see more strategic validity challenges to be filed as the commercial mRNA markets develop, especially since invalidity proceedings like IPRs are relatively inexpensive to pursue (e.g., estimated hundreds of thousands of dollars vs. district court litigations which could cost millions of dollars), while potentially yielding huge upside with respect to freedom to operate, depending on the markets involved.

Figure 8: Overview of mRNA IP and Competitive Landscape as of April 2021. N.B. the above overview and other information provided in Parts I, II, and III are in a constant state of flux and subject to significant ongoing change (e.g., market capitalization, opposition and IPR filings, regulatory candidates, alliances, etc. are all constantly changing and will continue to do so on an ongoing basis). This is one snapshot as of April 2021.

LNP and Other Delivery Systems are Critical to Commercialization

LNP and other related mRNA delivery technologies are linchpins for go-to-market commercialization, because mRNA sequences must be initially encapsulated in a delivery system to avoid being destroyed by the human immune system and effectively enter human cells. Delivery systems vary in technical composition and effect on the body, and each delivery system will therefore face different regulatory hurdles. LNP delivery systems, for example, do not have long regulatory track records; the first drug based on an LNP was approved by the FDA for a rare genetic disease in 2018. This limited regulatory history makes the process potentially more complicated for such systems.

Accordingly, the timing and success of mRNA candidate approvals may depend largely on the delivery technology used. If the delivery technology is unproven, the developer would likely need to vet with the regulators anew, which could take significant time. On the other hand, the same and previously-approved delivery system could be used for multiple different mRNA sequences directed to different indications. This could potentially speed up the approval process if the regulatory questions center on the new sequences and indication effectiveness, and not the safety of the delivery system, which would already be established.

It is therefore not surprising that mRNA market players have taken various approaches to secure LNP technology to use in connection with their own bespoke commercialization plans. For example, some companies in the space have developed their own tailored LNP technology to suit their candidates, some have in-licensed LNP technology, some have sought to invalidate competitor LNP delivery system patents to allow freedom of use, and still others have taken many or all of the above steps for a more diversified approach.

mRNA delivery technology has already raised several patent issues amongst competitors. In the case of Moderna, the company appears to have (at least previously) relied upon technology related to certain Arbutus LNP delivery systems but has also indicated it now has its own delivery technology and does not need a license from Arbutus to commercialize its products (including its COVID-19 vaccine). While reports suggest that approval of Moderna’s vaccine may have relied at least in part on preclinical data generated using technology covered by the Arbutus ’069 patent claims, Moderna has stated that the LNP delivery system it uses in connection with its commercial mRNA-1273 drug product is different.

The fact that Moderna was able to achieve speedy regulatory approval based on a new delivery system seems somewhat curious because regulators had undoubtedly required substantial data to justify clinical use of a new delivery technology. But Moderna’s pipeline is the largest amongst all market players, and Moderna presumably had the opportunity to vet its new LNP system with regulators well in advance of the COVID-19 outbreak, possibly as far back as 2016, when the company knew its license to the Arbutus LNP technology might have been in question.

Stephane Bancel, the CEO of Moderna, reportedly said that the company had innovated beyond the Arbutus LNP delivery technology because “We knew it was not very good,” “It was just okay,” he added. The company’s public statements support this proposition. In a recent SEC submission, Moderna stated that while it “initially used LNP formulations that were based on known lipid systems,” it “invested heavily in delivery science and ha[s] developed LNP technologies, as well as alternative nanoparticle approaches” to develop its own “proprietary” delivery systems. As for Moderna’s exact technology, when asked if Moderna would provide the molar ratios it uses for mRNA-1273 (its vaccine product), a Moderna representative said, “Nope, we are not disclosing our proprietary ratios at this time.” Perhaps these molar ratios and other details relating to Moderna’s delivery technology will be discovered during a patent infringement lawsuit between the companies.

BioNTech, on the other hand, appears to be in-licensing certain Arbutus LNP delivery technology. Whether it has a prominent home-grown delivery platform of its own upon which it currently relies for its medicines is not readily apparent. The result of Moderna’s appeal of its IPR against the ‘069 Arbutus patent therefore may have a significant impact on BioNTech if BioNTech is heavily relying upon the Arbutus LNP delivery technology covered by the ‘069 patent that may be affirmed invalid on appeal.

As for CureVac, its team is not embroiled in such controversies for its delivery technology at the moment and instead appears to have taken a diversified approach to its delivery systems. The German company has in-licensed LNP delivery technology from both Arcturus and Acuitas and also developed its own delivery technology called CVCM (CureVac Carrier Molecule). CureVac has indicated that “LNPs and CVCM delivery technologies complement each other in their applicability and enable us to cover a greater number of modalities within the mRNA space.” This diversified approach could prove wise, especially if different delivery technologies are needed for a variety of drug products and each technology is vetted by regulators separately, providing flexibility for commercialization of a broader range of candidates.

Translate BIO, Arcturus, and eTheRNA and Other Startups

With regard to Translate BIO and Arcturus, each is also well-positioned at the dawn of the commercial mRNA markets, and while these players are not as well-capitalized as Moderna, BioNTech, and CureVac, each has a market capitalization of over $1 billion, making them very large players in their own right. Although it is important to recognize that for all of these players, market capitalization is not necessarily an indicator of market strength, and much can change in a short period of time. As renowned economist Benjamin Graham is credited as saying; “In the short run, the stock market is a voting machine but in the long run, it is a weighing machine.” Each company will rise or fall on its own fundamentals.

Translate BIO is another pioneer in the mRNA space and has its own substantial patent portfolio and nearly ten products in the pipeline, with two in the clinic including a COVID-19 vaccine and a cystic fibrosis therapy candidate, while enjoying a strategic collaboration with Sanofi for infectious disease. The Lexington, Massachusetts-based company has independently developed its own LNP technology and in-licensed LNP technology from MIT and has apparently not sought to challenge competitor patents in IPRs or oppositions to date, at least publicly. Like CureVac, there is no public indication that Translate BIO in-licenses any of the legacy LNP patents from UPenn or that it needs to.

San Diego’s Arcturus has four drug candidates in its pipeline, with two in the clinic (one COVID-19 vaccine and one candidate for Ornithine Transcarbamylase Deficiency), and also has a large patent portfolio which is directed to, among other things, its LNP technology, which it licenses (at least in part) to CureVac. Like Translate BIO, it does not appear that Arcturus has filed any IPRs or oppositions against competitor patents to date (at least no public indication), and it is not clear whether Arcturus licenses mRNA technology from UPenn.

Finally, the emerging Belgian biotech company eTheRNA has a growing preclinical product pipeline and patent portfolio and apparently has developed its own LNP technology, all while interestingly being the smallest—but apparently most aggressive—market player against CureVac’s patents to date, filing eight oppositions against CureVac patents in Europe. Like several other market players, it is not clear whether eTheRNA has a license to UPenn’s mRNA technology.

Beyond eTheRNA, many other emerging companies exist in this space, including Sangamo Therapeutics, c?IMMUNE, Stemirna Therapeutics, Genevant Sciences, In-Cell-Art, Ethris, Tiba Biotechnology, ReCode Therapeutics, Strand Therapeutics, GreenLight Biosciences, Kernal Biologics, Inc., and others—with doubtless more to follow.

Such startups will likely drive growth in the mRNA technology market by finding new niche therapeutic areas to advance mRNA science and translation of that science with new therapies and concomitant new mRNA delivery technologies utilized for such new therapies. Accordingly, the opportunity for innovation and growth may dramatically increase for startups and existing market players, accelerated by further regulatory approvals, driving new mRNA therapies to treat and prevent disease.

Patent Litigation – Nothing Major to Report, Yet

While there are ongoing invalidity proceedings amongst these competitors, there have not been any major federal district court patent infringement litigations to date (save the Allele case against BioNTech and Pfizer discussed in Part I). This fact is not surprising because aside from the COVID vaccines, there are no other approved commercial mRNA products on the market, and presumably, companies would not want to be seen as hindering pandemic vaccination efforts by filing patent infringement lawsuits. The key players may be following the lead set by Moderna and its patent pledge for similar economic reasons as we’ve previously discussed.

Also, with a lack of other mRNA-based products on the market, much of the mRNA development activity amongst competitors remains secret and may also be covered under the 35 USC §271(e)(1) safe harbor clause, which exempts from infringement uses of third-party patents solely for uses reasonably related to the development and submission of information for regulatory approval. See, e.g., Merck KGaA v. Integra Lifesciences I, Ltd., 545 U.S. 193, 202 (2005). Accordingly, patent lawsuits may lack the proper basis to support infringement claims, and combined with lack of commercial sales, may be premature.

Nonetheless, with billions of dollars—and possibly more—at stake in the potential new mRNA markets, and despite Moderna’s October 2020 patent pledge, one would not expect the mRNA space to be litigation-free for long. Future regulatory approvals for new indications and newly-created drug markets will serve to drive the institution and scale of patent infringement actions, licensing deals, and merger and acquisition activity as new markets actualize.

Keep a Close Eye on Big Pharma

While the referenced pioneer companies have established themselves and grown considerably, it is important to keep an eye on big pharma. Several of the giants have already aligned with certain of the mRNA market players for an array of mRNA collaborations (e.g., BioNTech and Pfizer/Genentech/Sanofi; CureVac and Novartis/GlaxoSmithKline/Bayer; Moderna and Merck/AstraZeneca/Vertex; Translate BIO and Sanofi).

These collaborations themselves provide strong indications of big pharma’s interest and belief that mRNA could be critical to their bottom lines going forward. Pfizer’s CEO Albert Bourla has been even more direct, recently stating, “We like working with BioNTech, but we don’t need to work with BioNTech…We have our own expertise developed.”

This is a bold comment from the pharma giant and should cause all pioneer mRNA market players, not only BioNTech, to evaluate their leverage with respect to big pharma and others seeking to enter the U.S. and other markets independently with mRNA technology of their own or through the deals already in place.

Patent portfolios can provide valuable leverage, but not all patents are created equal, and the scope of an enforceable patent claim needs to be broad enough to cover competitor activities. Each mRNA pioneer should therefore evaluate their substantial patent portfolios to determine which existing patents are enforceable against other market players or potential market players upon commercialization.

mRNA pioneers should analyze their existing patent applications to determine whether broad claims can be written to cover current or anticipated competitor activity and should generate and file new applications and claims to that end also. This process will result in maximizing the leverage of each patent estate, which will be useful in enforcement activity, licensing deals, and set-up for exit through merger or acquisition. Now that mRNA is a viable commercial platform, pioneers possess more leverage when forging deals with big pharma and other collaborators, and pioneers should take these and other steps to maximize their market and negotiating positions in line with their overall strategic goals.

Perhaps Pfizer’s ominous comments directed to BioNTech are the first overture in a merger or acquisition play designed to expand its prowess in the vaccine market. Or GSK or Novartis, each with existing relationships with CureVac, may likewise merge with, acquire, or expand their relationship with CureVac to attempt to establish a dominant position in other mRNA spaces. Or perhaps Sanofi, already in deals with BioNTech, Translate BIO and Moderna, carves out its own position in the mRNA market by expanding capabilities through such partnerships and additional acquisitions (Sanofi acquired the mRNA startup Tidal for $470 million for “off-the-shelf” cell therapies for cancer, inflammatory diseases and potentially other conditions earlier this month).

Only time will provide the answers to these questions as the mRNA markets develop.

Global Healthcare Has Been Transformed

Finally, as we conclude this series of posts, we take a step back from mRNA market dynamics in the context of the first pandemic of our lifetimes in order to appreciate the bigger picture as applied to global health.

The manufacture, supply, and distribution of the COVID-19 vaccines may be by far the most significant undertaking for any drug—in any space—ever. Indeed, the vaccines are intended to reach nearly every human being on the planet, involve specialized handling equipment and protocols, and require unprecedented coordination with a multitude of governmental, private, non-governmental, and non-profit organizations around the world.

This process is now being executed, and it is remarkable to witness this happen in about a year from the time the virus was identified and mapped. If mRNA technology proves to be as groundbreaking as many expect, the global response rate to a future pandemic may be reduced even further, given how fundamentally different mRNA therapies are from traditional vaccines in terms of therapeutic approach and speed of synthesis, development, and scale. Of course, the largest rate limiter in getting effective mRNA drugs to patients—like other drugs—would be regulatory trials and approvals. It remains to be seen how regulators and developers may be able to accelerate the approval process even further in the face of another pandemic or other dangerous and widespread infectious diseases.

In any case, the new infrastructure will undoubtedly have a positive impact on global health in the longer term, including in the event of another pandemic, or to address other deadly infectious diseases that require widespread, worldwide or large regional distribution. The new infrastructure will also be useful for mRNA drugs in particular, including drugs directed to indications with relatively smaller patient populations, such as oncology, cystic fibrosis, and other dangerous diseases that require the unique mRNA and delivery system storage and delivery protocols and that will benefit from the established mRNA-ecosystem-based relationships.

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2026/07/Ankar-AI-Jul-30-2026-sidebar-700x500-1.jpg)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2026/07/Juristat-Varsity-Ad-2026-IPW-ad-FreeTrial_2-UPDATED-on-Jul-15-2026.png)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2026/07/ClearstoneIP-Varsity-Ad-2026-Ad-1.jpg)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2026/07/Womens-IP-Forum-2026-sidebar-register-early-bird-now-700x500-1.jpg)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2024/09/Patent-Prosecution-Training-sidebar-700x500-2025-03-27.jpg)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/WEBINAR-336-x-280-px.png)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/Ad-4-The-Invent-Patent-System™.png)

Join the Discussion

6 comments so far.

Javier

August 10, 2021 04:40 pmThis is great article. According to it, BNTX seems to use Arbutus LNP technology licensed by Genevant. I understand that license should be associated to a royalty. However, there is no mention about that royalty neither at BNTX, nor at Genevant nor at Arbutus. How long can usually this kind of royalty payments take?

hans-christian blom

May 3, 2021 03:59 amGreat series – thank you! Regarding the agreements with UPENN at least some of the financial terms have been disclosed in the forms you posted previously and in some press releases from both Biontech and Moderna. This is only part of the story though.

https://investors.modernatx.com/news-releases/news-release-details/moderna-provides-business-updates-and-reports-third-quarter-2019/

“Net cash used in operating activities includes $22.0 million and $25.0 million for the nine months ended September 30, 2019 and 2018, respectively, of in-licensing payments to Cellscript, LLC and its affiliate, mRNA RiboTherapeutics, Inc., to sublicense certain patent rights. After the first quarter of 2019, we have no further in-licensing payment obligations to Cellscript and its affiliate.”

anon

May 2, 2021 01:06 pmBioNTech is located in Mainz, Germany (DE “Deutschland”) just outside Frankfurt. GE is the country code for Georgia.

Anon

April 30, 2021 02:15 pm… the phrase “why buy the cow when you get the milk for free” seems woefully inadequate.

Anon

April 30, 2021 02:13 pmJosh,

Are you thinking that there would be a single “be all end all” patent?

You do realize that the Penn items date from well before COVID was in the scene, right?

I will add as a general note that this adds to the fire of complicated interwoven aspects that would draw “waiver” to be far more pernicious than merely any small number of “patent waiver.”

If indeed the non-patent extended know-how is also the target of waiver, you are looking at an extensive Post-Pandemic IP grab.

Josh Malone

April 30, 2021 10:18 amThis is very informative. I had been curious to know why there is so much fuss about march-in and waiver considering that Moderna and BioNTech both had rights to mRNA technology. This makes sense.

Now, this leads me to a new question. Why aren’t the UPenn sufficient to produce a COVID-19 vaccine? Or put another way, what utility did the UPenn patents enable?