“Implementers carry an extraordinary level of patent liability when reduced to licensing fees paid to third parties. These liabilities are why large Implementers have worked covertly to undermine the U.S. patent system.”

Nearly every operating company valued at greater than $20 billion in market capitalization is likely to be accused of patent infringement at some point. The high likelihood of utilizing another person or company’s patented technology led to an explosion of patent litigation activity over the last 30 years. Often, inventions emerge without a specific product in mind, and the strategy for the invention-turned-patent lacks a clear vision. This has been the way of invention since the patent offices were first formed and legal IP protection became a constitutionally ordained government program.

Nearly every operating company valued at greater than $20 billion in market capitalization is likely to be accused of patent infringement at some point. The high likelihood of utilizing another person or company’s patented technology led to an explosion of patent litigation activity over the last 30 years. Often, inventions emerge without a specific product in mind, and the strategy for the invention-turned-patent lacks a clear vision. This has been the way of invention since the patent offices were first formed and legal IP protection became a constitutionally ordained government program.

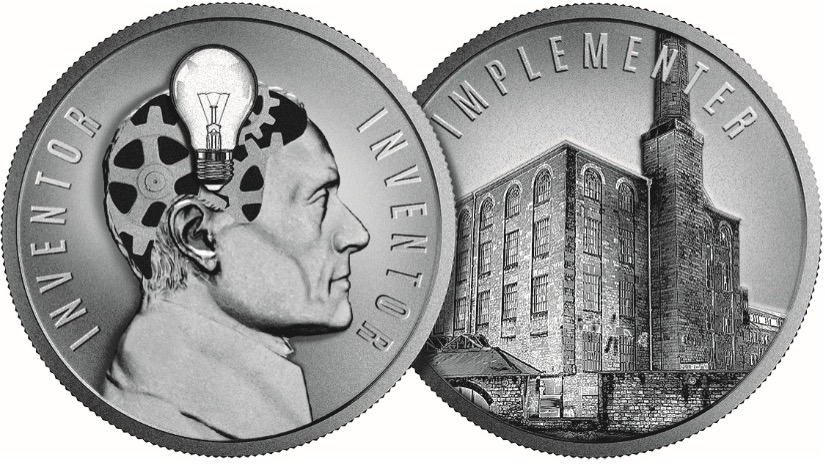

Nevertheless, invention is associated with the lightbulb, Thomas Edison’s iconic vision of a new idea. When the “lightbulb” goes on, creative ingenuity brings a new way of doing things, and a patent is a way to secure a financial profit on that idea, provided the Inventor knows how to commercialize the invention. Invention is one side of the Coin.

On the other side of the Coin are Implementers who build commercialized products. Expertise in commercialization is a uniquely different skill set from invention because business building requires interpersonal skills that are not always aligned with inventive skills. Said differently, Inventors are not always good at product development. As a result, Implementers with execution skills are known to push the boundaries of ethical in-licensing of others’ IP. The operational decision to sell products infringing on IP is a choice made by an Implementer, and one that is only policed by the patent owner.

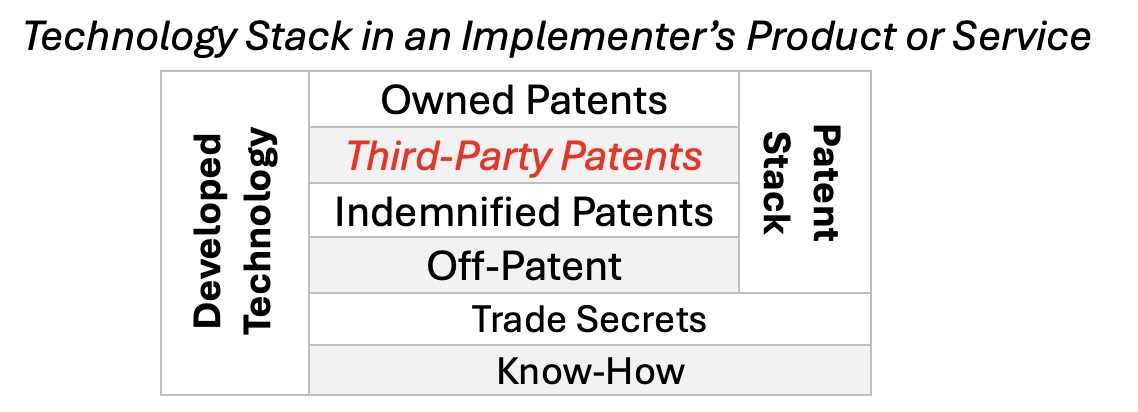

Implementers who execute business morally and ethically will launch new products with a freedom-to-operate (FTO) study completed before the launch of the new product. The FTO will indicate where patented technology exists within a product, allowing the company to determine how to deal with the third-party patented technology in its product. For patented technology identified in the FTO study, the implementing company could in-license the patented technology or design a work-around. Sometimes, patented technology in a product is indemnified through supplier parts and agreements, and a license is provided as part of the indemnification. Finally, and most importantly, the FTO will indicate the Implementers’ own patented technology used in its products and services. The full stack of technology in a product or service is categorized as follows:

The combination of patented technology in a product is called the “Patent Stack,” which is a subset of the total technology stack. A technology stack is like an ingredient list for a product’s technology, IP, and patents. The stack of patents is typically combined with enablement technology, such as trade secrets and know-how (i.e., people). The combination of patents, trade secrets, and employees’ know-how creates the intangible asset of Developed Technology, as defined in accounting terms.

While trade secrets and know-how are (generally) internally generated Developed Technology within a company, patented inventions are often developed simultaneously by competing groups. It is an inescapable fact. One that plagued Nathan Myhrvold, former Microsoft Chief Technology Officer and founder of Intellectual Ventures. During his early days at Microsoft in the 1990s, Nathan’s role included responding to patent holders’ requests for licenses. His issues at the time grew larger, and he is quoted in the book “Burning the Ships”:

“But Myhrvold soon realized just how deep Microsoft’s patent deficit actually was. ‘As Microsoft got bigger,’ he explains, ‘all sorts of companies started coming around to see us. They’d claim that we were infringing their patents, and demand that we take a license. And I was like, ‘Oh my God, they can do this? They can just demand money from us?’’ A lot of people were shocked by that, I can tell you. And when our lawyers looked around and asked what sort of patents we could assert back against these companies—in a sort of ‘mutual assured destruction’ show-down that would enable us to cross-license without having to fork over a lot of money—the answer was, ‘We don’t have crap.’ So every time one of these companies came by to assert their patents against us, it would cost us money. Sometimes 50 or 100 million dollars. And that’s a lot of zeroes to give away just because someone else (has patents).”

Nathan’s dawning realization of vast infringement at Microsoft was not isolated to Microsoft. Throughout the 2000s, Big Tech companies have had a deficit of owned patented technology covering their products. The technological explosion that accompanied society’s adoption of the Internet led to an unprecedented number of patents being applied for and granted. With patent issuance on the rise, companies, big and small, were being sued for patent infringement during the late 1990s and early 2000s. The rise of “patent trolls” led to the most significant legislative reform to the patent system in decades. The America Invents Act (AIA) transformed how the patent system operates, and has ushered in an era of efficient infringement, the act of using another patent holder’s technology without compensating the patent holder for its use.

Patent Liability: The Financial Exposure

Paying third-party patent licensing fees lowers earnings per share (EPS). It causes Chief Financial Officers (CFOs) to lower earnings expectations to Wall Street financial analysts. It is an uncertain event that creates havoc for public companies that need certainty and sustainable revenue and profits. To that end, most Big Tech IP departments are tasked with figuring out how NOT to pay patent licensing fees. This makes for an incredibly tricky problem for alleged infringers. Implementers accused of infringement rely upon a wide variety of methods to undermine patent litigations.

Unfortunately for Implementers, patented inventions accumulate within an Implementer’s product, creating products that incorporate hundreds, if not thousands, of patents. These patents are either owned or not owned by the implementing company, and understanding which patents are the ingredients that make up a product is defined through a freedom-to-operate (FTO) study. Once the FTO study is completed, determining a reasonable royalty for internally generated vs. third-party licensing rates is possible. But how? More importantly, who would be willing to disclose such a figure?

The answer is recently acquired companies through corporate mergers and acquisitions (M&A). The financial reporting guidance under generally accepted accounting principles (GAAP) requires companies to value its Developed Technology and place the value on its balance sheet. This accounting rule was born out of a few notable events that uniquely shaped the IP valuation world:

- the Dot Com bubble popping from 2000 to 2002,

- Enron’s financial collapse in 2002, and

- the failure of Arthur Anderson, one of the former Big 5 accounting firms.

Due to the financial disruptions from those events, which caused significant economic harm, Congress passed the most comprehensive regulatory accounting changes in decades, known as the Sarbanes-Oxley Act (SOX). SOX altered how companies account for acquired assets in M&A. The old and simplistic methods of “pool” accounting for combined companies were wildly inaccurate relative to the Fair Value of an acquired company’s assets. When SOX became law in 2002, almost overnight, a nascent finance industry of business and intangible asset valuation practitioners emerged.

IP and intangible asset valuation is a human algorithm that ties together a myriad of unlikely data and structures it into a financial estimate. Accurate valuations have a strong tie to price, and IP does not have a meaningful transaction market by which to reconcile value vs. price. Accordingly, debate and disagreement between reasonable people about the value of IP create an underlying tension. The tension that exists when presenting IP asset value is a lack of credibility. Are you able to take the valuation estimate provided and turn it into a transactable price for the IP asset? Will the IP asset value hold up in a liquidation scenario? More often than not, the answer is no.

Valuing IP is not for the faint of heart. It is exceedingly difficult, yet vitally important to IP owners. However, the AIA has made it nearly impossible to accurately calculate the value vs. price of IP and patent assets. Creating an active IP marketplace that includes disclosure of IP monetization transactions is a linchpin to accurately valuing IP. Without an active IP marketplace, accurately valuing IP becomes exceedingly difficult.

Patent Licensing Hold-Out Skews Patent Values

Patent hold-out explains what an Implementer does when a patent holder requests a license from the Implementer, and the Implementer delays or refuses to compensate the patent holder for unauthorized use. In most cases, the Implementer can continue selling its alleged infringing product, but holds out from paying licensing fees until compelled to do so through the court system. Often, an Implementer that loses a patent litigation can continue to delay paying patent fees through the entire appeal process through the U.S. Court of Appeals for the Federal Circuit. As an Implementer, holding out is the prudent course of action and is in the best interests of the Implementer’s investors.

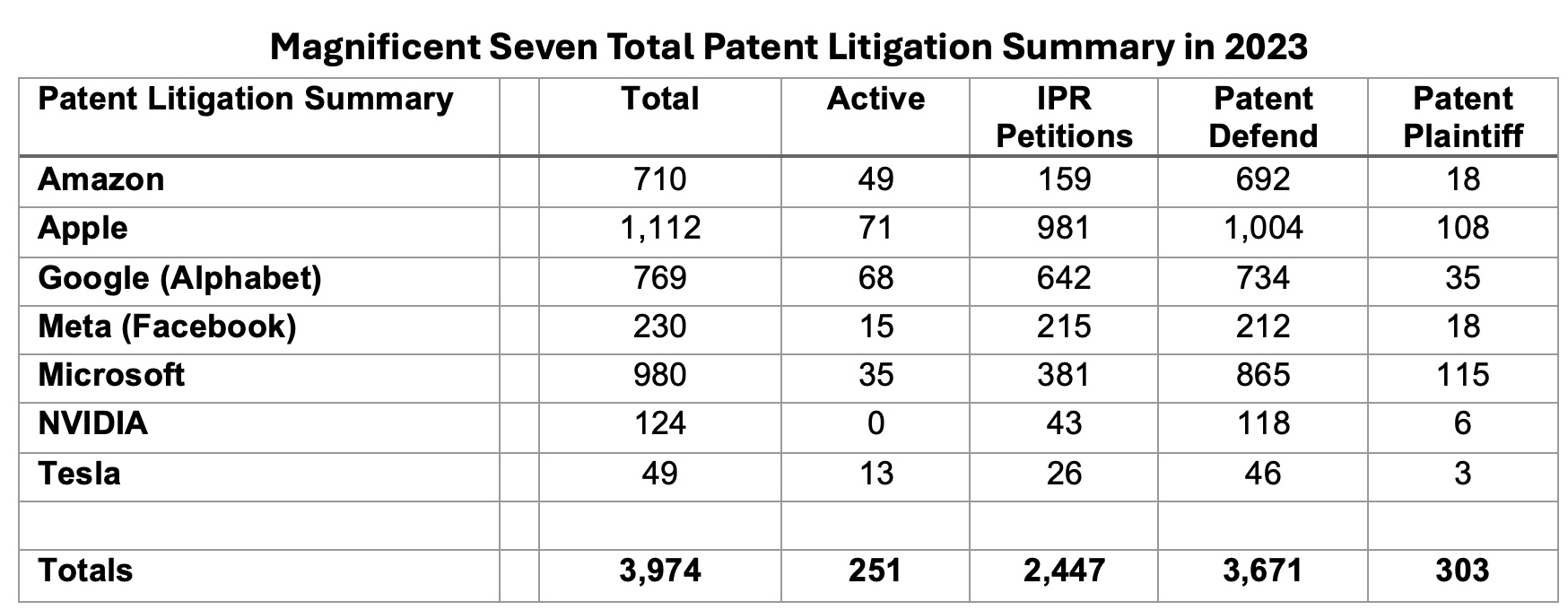

The world’s most famous Implementers are the “Magnificent Seven.” These companies, whose market capitalization has exceeded $1 trillion, include Amazon, Apple, Alphabet (Google), Meta (Facebook), Microsoft, NVIDIA, and Tesla. These seven companies represent the world’s largest collection of “alleged” patent infringers.

The Magnificent Seven has incredible exposure to patent litigation, with over 3,670 patent litigations (and counting) filed against the seven in 2023 (the latest information freely available through RPX Insights). Unsurprisingly, the Magnificent Seven were the biggest beneficiaries of the efforts to enact the AIA. As a result, the Magnificent Seven are leaders of invalidating third-party patents. Here’s a summary related to patent litigation as of year end 2023:

While the number of patent assertions against the Magnificent Seven is staggering, so too are the revenue figures of the combined seven at $1.8 trillion in 2024. Amazingly, revenue for the Magnificent Seven is estimated to grow to $3.5 trillion by 2030. With that much control of the U.S, and global economy in seven companies, it stands to reason that they would uphold the highest ethical standards regarding utilizing other entities’ patented technology, but the numbers tell the actual story.

The Magnificent Seven companies are defendants in hundreds of active patent litigation cases. In a direct correlation, the same seven companies actively work to invalidate the patents asserted against them, highlighting their attempt to kill (and thus avoid paying for) other Inventors’ work. But why do these companies fight so hard to protect their developed technology while invalidating another person’s patents? The simple answer is profits. Not paying patent licensing fees improves profitability; therefore, do everything possible not to pay patent licensing fees.

So, how much are the Magnificent Seven saving by acting obstinately about paying third-party patent licenses? I’ve made an estimate using a simplistic formula and then back-solved to ensure the outcomes were reasonable.

In the most simplistic terms, a tiny sliver of a royalty rate can be carved out of the revenues and allocated to the varied entities accusing the Magnificent Seven of patent infringement. Even at the most conservative estimates, paying royalties of 0.1% to 0.2%on revenues will result in billions of dollars in patent licensing fees paid to third-party patent owners. Of course, the actual royalty rates will vary on a case-by-case basis, but for simplicity, these estimates explain why the fight over patents is so significant.

Implementers carry an extraordinary level of patent liability when reduced to licensing fees paid to third parties. These liabilities are why large Implementers have worked covertly to undermine the U.S. patent system. Further, the exposure to patent liabilities is universal across all companies with more than $20 billion in annual revenue, which is why intransigence towards other people’s patents is the standard response from all Implementers.

In consideration of the patent liability, a great issue becomes exposed: I estimate the financial liability to third-party patent owners by the Magnificent Seven to be $16.7 billion to $33.5 billion in potential value lost that should be transferred to patent owners over the next eight years.

That is a staggering figure, based solely on 0.1% to 0.2% of revenue. By denying the payment of patent licensing fees, value accrues to the Magnificent Seven through “trickle-up” economics.

This article is an excerpt from the author’s forthcoming book, The Venture Capital Alternative.

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2026/02/LexisNexis-Mar-31-2026-sidebar-700x500-1.jpg)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/WEBINAR-336-x-280-px.png)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/Ad-4-The-Invent-Patent-System™.png)

Join the Discussion

No comments yet. Add my comment.

Add Comment