“Patent filings across technology clusters and applicant countries remain remarkably stable for the large- and small-molecule industry.”

This is the eighth in a 13-part series of articles authored by Kilpatrick Townsend that IPWatchdog will be publishing over the coming weeks. The series will examine industry-specific patent trends across 12 key patent-intensive industries.

In our last article exploring patent trends across 12 industries, we addressed the industrial design industry. To quickly summarize this series and the underlying study (performed in a collaboration between Kilpatrick Townsend and GreyB Services):

- The goal of the research was to characterize recent patenting trends and statistics for each of twelve industries (and technology clusters within those industries) to inform applicants’ filing decisions of tomorrow.

- The study was conducted at an industry level (not at an art-unit or class level). This was achieved by designing and implementing various queries and iteratively manually reviewing a large number of search results to refine the queries.

- The study is further unique in that we used proprietary data from recent years and data-science techniques to estimate statistics for recent time periods (which would otherwise have poor data as a result of the non-publication time window).

Today’s article pertains to the therapeutic and diagnostic molecules industry. Few other industries have the potential to so dramatically affect individuals’ lives as does this industry. While on a day-to-day basis it can be easy to forget the intensive bench work and clinical trials that are being undertaken in attempts to better treat or cure disease, it is this steady pulse of investment and effort that has led to the cure of many ailments and diseases. Rather recently, biologics advancements have expanded the field to no longer merely rely on small-molecule compositions but to draw upon a large pool of sophisticated large-molecule options. However, research and development in the pharmaceutical space remains heavily regulated and extraordinarily expensive. Thus, investments must be chosen and protected wisely.

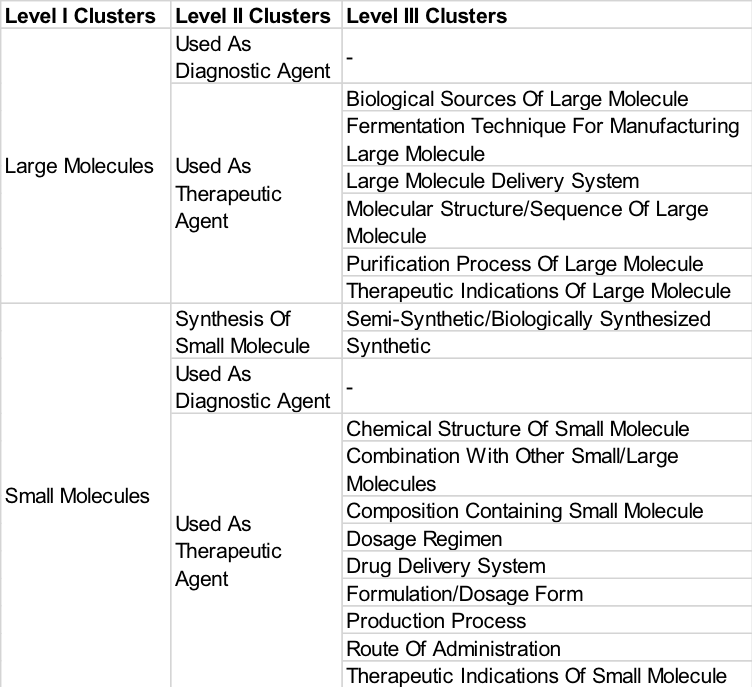

Our study not only identified a set of applications that pertained to this industry, but also—for each application in this set—we determined whether the application pertained to one or more of the categories shown in the topology below. If so, the application was appropriately tagged, such that it could be included in one or more category-specific data subsets for subsequent analysis.

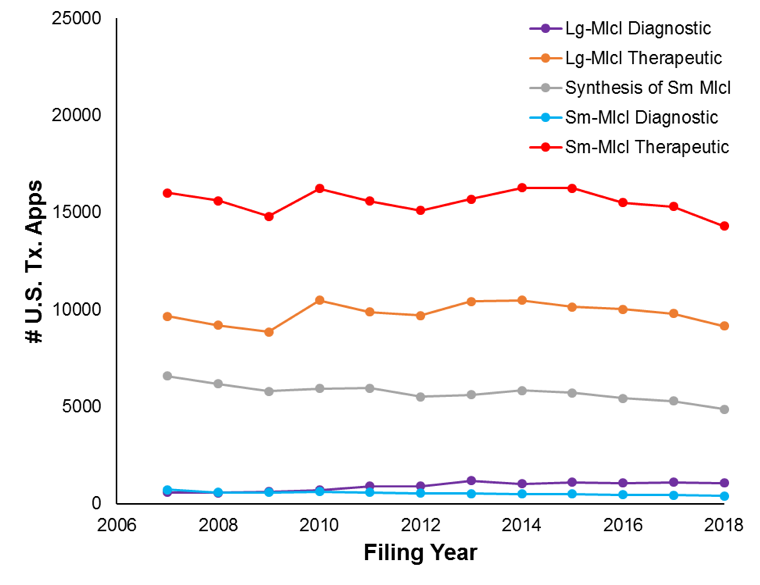

As reported in our initial patent trends article, filings for the industry overall have remained rather steady over the studied time period: from approximately 22,700 filings in 2007 to approximately 21,300 filings in 2018. Figure 1A shows the filing trends broken down by Level-I Clusters.

Figure 1

Thus, therapeutics filings dominate over diagnostic filings. Further, despite the fact that biologics are relatively new, small-molecule filings are substantially higher than large-molecule filings. This may be due to the fact that small-molecule filings can use chemical structures with “R” groups which can be broadly defined, such that a high number of compounds are covered. Meanwhile, large-molecule filings are much more specific. Thus, if a patent application is filed somewhat early during research efforts, there may be a higher chance that the application would cover the effective drug if it is a small-molecule filing as compared to if it is a large-molecule filing. Companies may thus be more inclined to file more small-molecule applications at earlier R&D stages as compared to large-molecule applications.

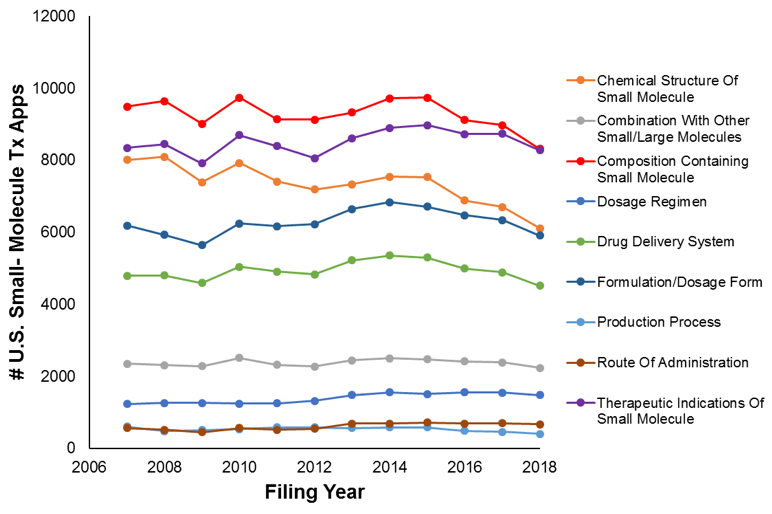

Figures 2A and 2B show filing trends across Level-II clusters within the small-molecule diagnostic cluster and large-molecule diagnostic cluster, respectively.

Figure 2A

Figure 2B

For both large molecules and small molecules, the prominent type of filing pertains to the structure (or sequence) of the molecule. The second most prominent filing type (for both small and large molecules) pertained to the therapeutic indications (e.g., method of use) of the molecule.

Across all level-II clusters, filing counts were relatively stable. However, some movement was observed within the large-molecule clusters (e.g.,, with the delivery-system applications increasing by 14% and the therapeutic-indication filings increasing by 12%). The more dramatic changes in the large-molecule cluster is perhaps unsurprising given that the large-molecule field is newer than the small-molecule field.

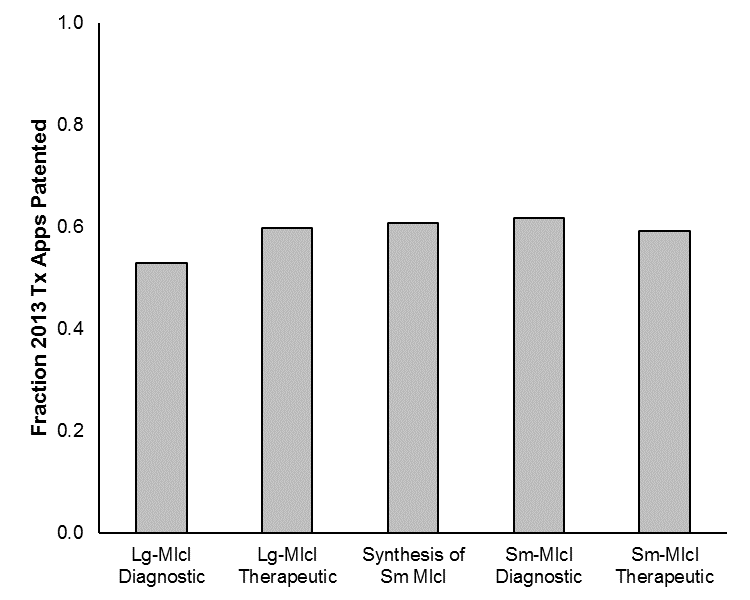

Figure 3 shows, for each of the Level-I clusters, the fraction of the applications that were filed in 2013 and are now patented. Notably, the percentages are rather similar, with the exception of large-molecule diagnostics (which is associated with a slightly lower patenting rate). Within these categories, the percent patented within the small-molecule chemical structure cluster is 67% and is 63% for the large-molecule molecular structure/sequence cluster. Further, the percent patented for the therapeutic-indications cluster for the small molecules and for the large molecules is 60% and 58%, respectively.

Figure 3

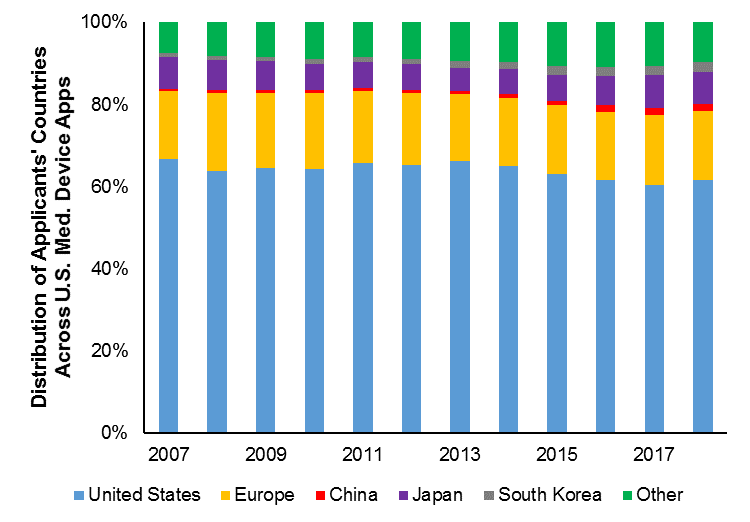

Figure 4 shows a time-series breakdown of applicants’ countries. The contribution of U.S. applicants to U.S. filings in the therapeutic and diagnostic industry has been slightly increasing. This is interesting given that, for most other industries in our study, U.S.-applicant filings were substantially increasing, yet the contribution percentage was falling. Here, even though the U.S. filings are approximately constant, the contribution percentage has not fallen.

Figure 4

Patent filings across technology clusters and applicant countries remain remarkably stable for the large- and small-molecule industry. This stability may speak to the regulatory hurdles, long development cycles and expense associated with developing a therapeutic for this industry. Without these expenditures over a lengthy time period, a company may fail to identify a valuable composition (or formulation, etc.) and/or may fail be able to set up the composition to be brought to market. Thus, any patent secured may thus be ill-focused or of little value. Nonetheless, given that successful pharmaceuticals can be worth tens of billions of dollars, failing to file patent applications on legitimate prospects would be a costly mistake as generics would immediately undermine the lost exclusivity. It appears that, for the time being at least, applicants have reached a steady state on filing.

A copy of the full published study is available with additional detail here.

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2024/04/Patent-Litigation-Masters-2024-sidebar-early-bird-ends-Apr-21-last-chance-700x500-1.jpg)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/WEBINAR-336-x-280-px.png)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/2021-Patent-Practice-on-Demand-recorded-Feb-2021-336-x-280.jpg)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/Ad-4-The-Invent-Patent-System™.png)

Join the Discussion

2 comments so far.

D

May 14, 2019 06:32 pmWhile the number of applications may be similar to a decade ago, what jumps out at me from the graphs is the downward trend over the last 4-5 years.

Anon

May 10, 2019 02:27 pmNot nearly the drop-off that I was expecting.