“While patent filings are greatly increasing in a number of tech industries, filings are plateaued or falling in others. This difference may be partly explained by allowance-rate distinctions.”

This is the first in a 13-part series of articles authored by Kilpatrick Townsend that IPWatchdog will be publishing over the coming weeks. The series will examine industry-specific patent trends across 12 key patent-intensive industries.

Companies are frequently faced with high- and low-level decisions concerning patenting. What should an annual patent budget be and/or how many new applications should be filed each year? Which technologies should be emphasized in the portfolio? For a given innovation, should a patent application even be filed? These questions are frequently evaluated by looking at internal factors, such as recent enterprise-wide profitability, executive sentiments towards patenting, and/or the perceived importance of individual projects.

However, the effect of a patent is to exclude others from a given innovation space. If no other entity was or would be interested in making, using, selling, or importing a patented invention, one could argue that the patent was valueless. Conversely, if many others are actively developing technology within a space, a patent portfolio in that area may be particularly valuable.

Thus, patenting decisions should factor in the degree to which others have interest in a given technology is trending-up or -down. Patenting data can serve as one indicator for this type of interest. However, it is difficult to collect patenting data at an industry level. While the patent office assigns an art unit and a class to each patent application, using one or more art units and/or classes as a proxy for an industry is both under- and over-inclusive. For example, a patent application related to an Internet of Things (IoT) industry may also relate to traffic lights, such that, even if there were art units specifically and only associated with either IoT or traffic lights (which there is not), statistics would be inaccurate: statistics pertaining only to an IoT art unit would not account for data corresponding to applications and assigned to the hypothetical traffic-light art unit, while statistics pertaining to both art units would be based on non-IoT applications assigned to the latter art unit.

Meeting the Challenge

Collecting industry-level patenting data is therefore not an easy task. However, given the value of this data, Kilpatrick Townsend has partnered with GreyB Services to collect this data. We studied 12 industries: artificial intelligence (A.I.), IoT, medical devices, computational biology and bioinformatics, therapeutic and diagnostic molecules, wireless phones, industrial design, FinTech, CleanTech, building materials, blockchain, and automotive. For each industry, an application data set was collected by iteratively defining and running search queries and performing extensive manual reviews of results of the search queries. The data was limited to applications filed in the U.S. from 2007 onwards with hundreds of thousands of patent families.

One complexity with patent data is that applications are not published until 18 months from their priority date, and some applications (filed with non-publication requests) do not publish unless and until they are issued as patents (or the non-publication request is withdrawn). To address these realities, we collected a proprietary data set that included high-level patenting indicators and deep learning algorithms. We derived relationships between this data set and industry-specific filing counts outside of the non-publication window, and then we generated filing-count estimates for 2017 and 2018 for each industry.

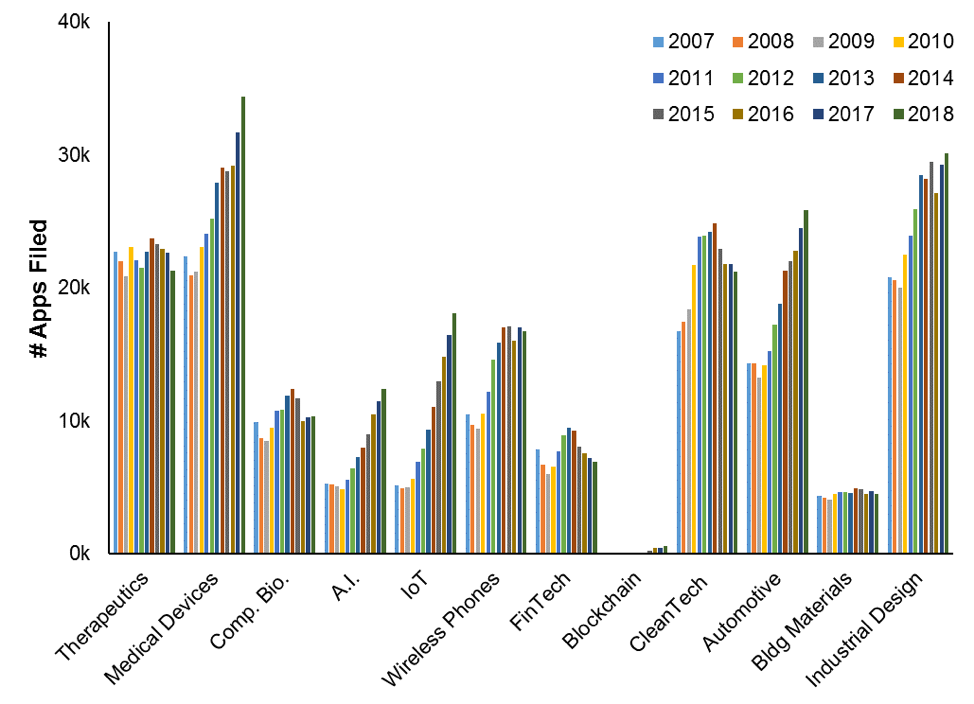

Figure 1 shows the year-after-year U.S. filing counts per industry. While patent filings are greatly increasing in a number of tech industries, filings are plateaued or falling in others. This difference may be partly explained by allowance-rate distinctions. More specifically, sharp increases in filings were observed for some of the industries: medical devices, AI, IoT, blockchain and automotive. These filing explosions may be consistent with substantial advancements and corporate prioritization of these industries seen in recent years.

Figure 1

Filings in the wireless-phone and industrial-design areas had been dramatically increasing in the early part of the time period but have recently plateaued. In the building-materials and therapeutic-and-diagnostic-molecules industries, filings have been rather stable across the years studied. Potentially, this stability is due to high costs of entry into the industry, such that it is less likely that new players will enter the industry and contribute new ideas. Further, each of these industries is highly regulated. Thus, because new treatments and new building materials may require extensive and expensive testing before they can be marketed, applicants may be more selective about their patent filings.

In the computational-biology, FinTech and CleanTech industries, filings had increased until 2014, after which they fell off. Notably, Alice v. CLS Bank was decided in June 2014, after which it became more difficult to patent business-method and bioinformatics patent applications. The recent filing decrease for FinTech and computational biology may represent applicants’ frustrations with attempting to secure patent protection in these areas and/or having limited budgets for new filings given the extended prosecution of pending applications.

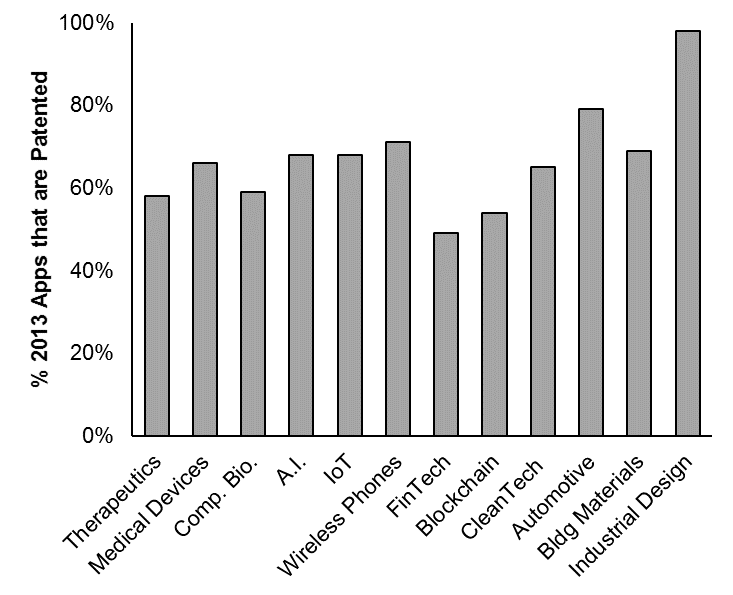

Figure 2 shows the percentage of industry-specific applications filed in 2013 that are now patented. Generally, for industries in which filings have recently decreased (e.g., FinTech, computational biology), the allowance prospects are lower than for other industries. However, the correlation is not perfect. For example, blockchain’s patenting percentage is quite low, but filings have been solidly increasing for this industry.

Figure 2

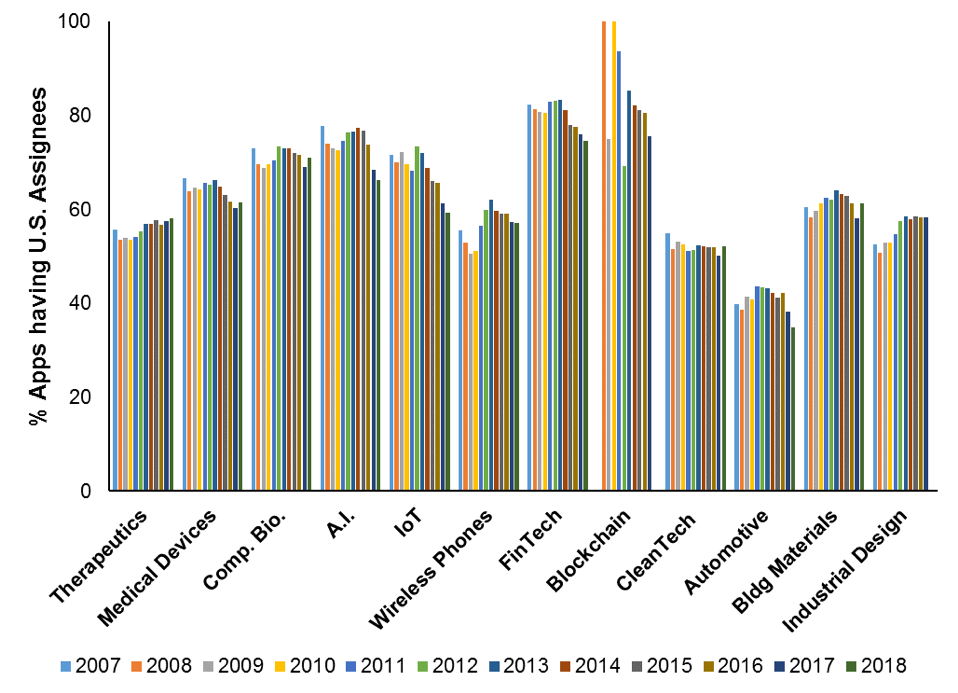

For each application in the data set, the country of the assignee was identified. Figure 3 shows the percentage of applications filed in each year since 2007 and for each industry corresponding to U.S. assignees. A decreasing contribution of U.S. assignees is observable across many industries. This decrease does not necessarily indicate that U.S. entities are filing fewer applications in the industry, but just that the rate of change of filings from non-U.S. assignees is greater than that for U.S. assignees so we might be losing our prior innovation advantage. Such a result may be due to foreign enterprises increasing prioritization of securing international portfolios as a result of globalization.

Figure 3

A topology was defined for each industry, in which different categories within individual industries were defined. Each application in our data set was tagged using the topology, so as to indicate each category to which it is associated. In subsequent days, we will be publishing drill-down data on IPWatchDog for each industry using these topologies, such that trends and hot areas within each industry can be identified. Applicants can therefore use this data not only to inform their high-level patenting strategy (e.g., amount of patent applications to be filed) but also to inform their detailed strategies (e.g., to identify which types of innovations to prioritize for patent protection). A copy of the full published study is available with additional detail here.

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2024/04/Patent-Litigation-Masters-2024-sidebar-early-bird-ends-Apr-21-last-chance-700x500-1.jpg)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/WEBINAR-336-x-280-px.png)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/2021-Patent-Practice-on-Demand-recorded-Feb-2021-336-x-280.jpg)

![[Advertisement]](https://ipwatchdog.com/wp-content/uploads/2021/12/Ad-4-The-Invent-Patent-System™.png)

Join the Discussion

No comments yet.